How is your credit score calculated?

Your credit score plays a huge role in your financial life, yet so many of us don’t learn how it actually works until we run into trouble. It’s a three-digit number that tells lenders how reliable you are when it comes to borrowing money. In Canada, credit scores range from 300 to 900—the higher, the better. But what exactly goes into calculating that number? I’m going to break it down in simple terms so you can take control of your credit with confidence.

IN THIS ARTICLE

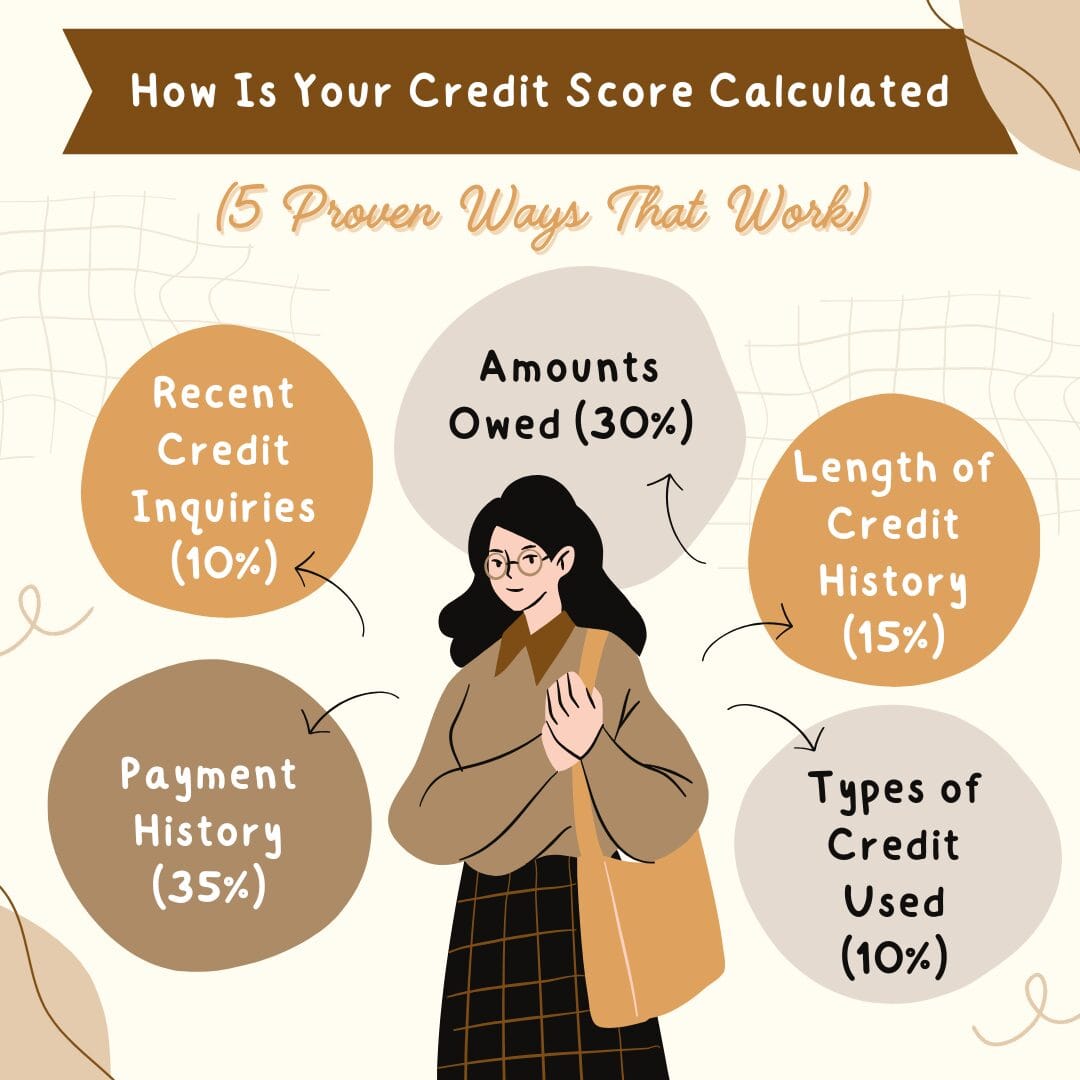

How Is Your Credit Score Calculated (5 Proven Ways That Work)

1. Payment History (35%) – The Most Important Factor

This is the big one. Lenders want to know if you pay your bills on time. Late payments, defaults, or accounts sent to collections can seriously hurt your score. So, always aim to pay at least the minimum amount due on time. Lenders want to see that you’re reliable. Late payments signal risk.

📌 How to improve:

- Set up automatic payments or reminders.

- Pay at least the minimum due, but ideally in full.

- Avoid collections by settling debts before they escalate.

2. Amounts Owed (30%) – Credit Utilization

This is also called credit utilization—basically, how much of your available credit you’re using. Maxing out your credit cards? Not a great idea. Aim to keep your balances low, ideally under 30% of your limit. A high balance can make it look like you’re relying too much on credit or under financial stress, which isn’t a good sign to lenders.

📌 How to improve:

- Keep credit usage under 30% of your limit (e.g., if your limit is $10,000, keep the balance under $3,000).

- Pay off high-interest debt first (credit cards usually have the highest rates).

- Increase your credit limit (but don’t spend more).

3. Length of Credit History (15%) – How Long You’ve Had Credit

The longer you’ve been using credit responsibly, the better. This factor looks at how long your credit accounts have been open. A longer credit history shows you’ve got experience managing credit wisely. If you’re new to credit, don’t worry—it just takes time to build it up!

📌 How to improve:

- Keep old accounts open (if they have no fees).

- Avoid frequently opening and closing credit accounts.

4. Types of Credit Used (10%) – Credit Mix

Having a mix of credit types—like credit cards, car loans, and a mortgage—can show lenders you’re capable of managing different kinds of debt. But don’t open new accounts just for the sake of diversity; only take on credit you need. Lenders prefer borrowers who can manage different types of debt.

📌 How to improve:

- A mix of credit types (but only if needed) can help build your score.

- Don’t open new accounts just to boost this factor—it’s less important than payment history and utilization.

5. Recent Credit Inquiries (10%) – Hard Inquiries from New Applications

Every time you apply for credit, a “hard inquiry” is recorded. Too many of these in a short period can make you look risky and desperate to lenders. It’s okay to shop around for the best rates, but try to do so within a short timeframe to minimize the impact.

📌 How to improve:

- Only apply for credit when necessary.

- Rate shopping (for mortgages or car loans) should be done within a short period (usually 14-45 days) so multiple inquiries count as one.

- Check your credit report regularly to ensure no unauthorized inquiries.

Common Questions About Credit Scores

Does checking my own credit score hurt it?

Nope! When you check your own score, it’s considered a “soft inquiry” and doesn’t affect your score. It’s actually a good idea to monitor your credit regularly.

How long do late payments stay on my report?

Late payments can stay on your credit report for up to six years, but their impact lessens over time, especially if you make consistent on-time payments afterward.

Will closing old credit cards improve my score?

Not necessarily. Closing old accounts can shorten your credit history and increase your credit utilization ratio, both of which might lower your score. If there’s no annual fee, it might be better to keep them open.

Can I improve my credit score quickly?

Improving your score is more of a marathon than a sprint. Paying bills on time, reducing debt, and not applying for too much new credit at once are steady steps toward a better score.

Remember, your credit score is a reflection of your financial habits. By learning what impacts it and making informed choices, you’ll be on the path to a healthier financial future.

Related Reads…

Resources

TransUnion – What Affects Your Credit Score?

Equifax – How Are Credit Scores Calculated?

Government of Canada – Improve Your Credit Score

Investopedia – How to Rebuild Your Credit

Discover more from The Unscripted Femme

Subscribe to get the latest posts sent to your email.